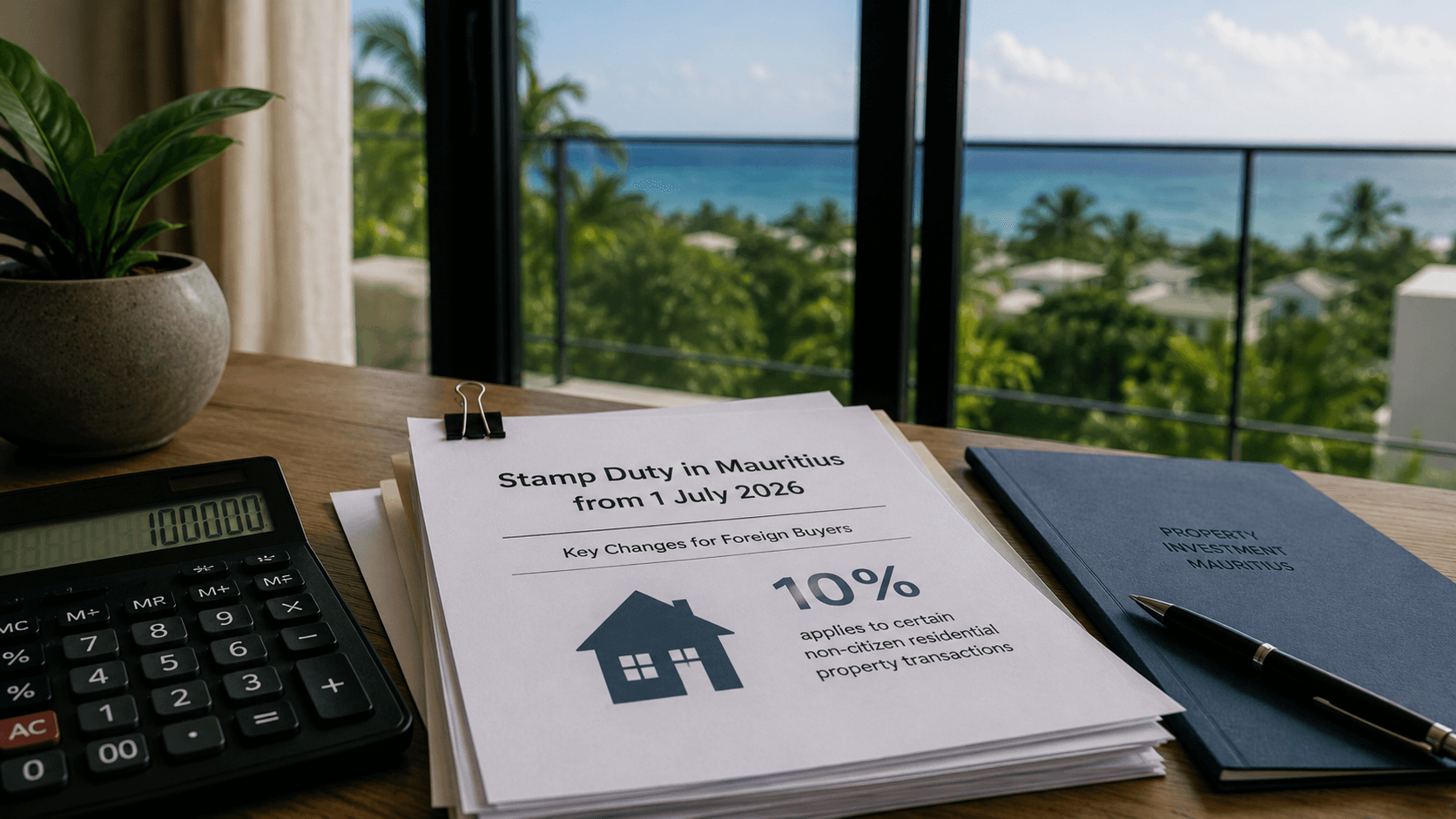

Registration Duty in Mauritius for Foreign Buyers from July 2026

From 1 July 2026, some non-citizen residential property purchases in Mauritius may face 10% registration duty. Check before signing.

Registration duty in Mauritius for foreign buyers becomes especially important from 1 July 2026, when a 10% rate applies to certain non-citizen residential property transactions. For buyers, the key point is not only the rate itself, but whether the transaction falls within the scope of the rule.

Registration duty is one of the acquisition costs that should be understood before signing a deed of sale. It can affect the total amount required to complete a purchase, especially where the buyer is a non-citizen and the property falls under an approved acquisition route.

This article explains what registration duty is, when the 10% rate may apply from July 2026, and what foreign buyers should check before committing to a property purchase in Mauritius.

For a broader view of the acquisition timeline, our article on the property buying process in Mauritius for foreign buyers explains how approval, payment structure and registration fit together.

What is registration duty in Mauritius

Registration duty is a duty payable when certain legal documents are registered. In a property transaction, it is usually linked to the registration of the deed witnessing the transfer of the property.

For a buyer, registration duty is part of the acquisition cost. It is separate from notarial fees, agency fees, bank charges, financing costs, currency conversion costs and other transaction-related expenses.

The notary usually plays a central role in calculating the amount payable, collecting the required sums and completing the registration process. However, foreign buyers should still understand the principle before signing, especially where a transaction may be affected by the July 2026 changes.

Registration duty should therefore be included in the buyer’s budget from the beginning, not discovered only at the final signing stage.

When the 10% rate applies from July 2026

The 10% registration duty should not be described as a blanket rule for every foreign-buyer transaction. It applies to specific transactions set out in the legal framework.

From 1 July 2026, the 10% rate applies to the registration of a deed witnessing the transfer to a non-citizen of certain residential property. This includes residential property under an EDB Property Scheme or under a relevant route in the Non-Citizens (Property Restriction) Act, including certain residential properties first acquired under those routes.

In practical terms, this may concern properties acquired by non-citizens under approved frameworks such as PDS, IRS, RES, Smart City Scheme, IHS or qualifying apartment routes, depending on the specific transaction and legal structure.

For a broader comparison of these approved acquisition routes, see our article on property investment schemes in Mauritius.

Foreign buyers should not rely on general statements such as “foreigners pay 10%”. The safer question is: “Does this specific transaction fall within the 10% registration duty rule from 1 July 2026?” That answer should be confirmed by the notary before signature.

For a broader view of the 2025 Budget changes affecting foreign buyers, our article on Mauritius Budget 2025 for foreign buyers explains the key measures to review before signing.

Why the date matters

The date matters because the 10% rate applies to in-scope transfers to non-citizens on or after 1 July 2026.

This is especially important for buyers whose transactions are close to the changeover date. A reservation, preliminary agreement or commercial commitment may not be enough to determine the final registration duty if the deed is completed or registered later.

Foreign buyers should confirm:

the expected date of signature;

the expected date of registration;

whether the 1 July 2026 date affects the transaction;

whether any delay could change the applicable duty;

whether the notary has confirmed the rate for the specific deed.

This is particularly relevant for off-plan or VEFA-style purchases, where there may be a longer timeline between reservation, staged payments, deed signature, completion and registration.

Registration duty is not land transfer tax

Registration duty and land transfer tax are often mentioned together, but they are not the same thing.

Registration duty is generally part of the acquisition-cost discussion for the buyer. It relates to the registration of the deed and should be included in the buyer’s completion budget.

Land transfer tax is generally associated with the seller side of the transaction. However, it can still affect the wider negotiation, pricing and resale context, especially when new rates apply to certain non-citizen property transactions.

For clarity, buyers should ask their notary to separate:

registration duty;

notarial fees;

agency fees where applicable;

bank and currency conversion costs;

any seller-side taxes that may affect the transaction context;

other transaction-specific charges.

This makes the real cost of acquisition easier to understand.

How this affects foreign-buyer budgeting

A 10% registration duty can materially affect the total amount required to complete a purchase. Foreign buyers should therefore avoid assessing affordability based only on the advertised property price.

A realistic acquisition budget should include:

the purchase price;

registration duty;

notarial fees;

possible agency fees;

bank charges;

currency conversion costs;

financing costs where applicable;

project or scheme-specific costs where relevant.

The impact may be particularly important for buyers who are:

purchasing close to the 1 July 2026 changeover date;

buying under an approved property scheme;

buying off-plan or under a VEFA structure;

transferring funds from abroad;

planning a residence-permit-linked acquisition;

working with a fixed budget in foreign currency.

Exchange rates can also affect the real cost for foreign buyers. Even where a property is marketed in a foreign currency, the payment mechanics, conversion treatment and duty calculation should be confirmed before signing.

What buyers should ask before signing

Before signing a deed of sale or committing to a purchase timeline, foreign buyers should ask clear questions about registration duty.

Useful questions include:

Is the buyer treated as a non-citizen for this transaction?

Does the property fall under an EDB Property Scheme or another in-scope route?

Is the 10% registration duty rate applicable to this transaction?

What is the expected deed registration date?

Could a delay affect the applicable duty?

How is the property value assessed for duty purposes?

Are notarial fees and registration duty calculated separately?

Is land transfer tax relevant to the seller?

Are bank charges, agency fees and currency conversion costs included in the estimate?

Has the notary provided a full transaction-specific cost breakdown?

These questions help buyers understand the real completion cost and avoid surprises before the deed is signed.

What this means for off-plan and VEFA purchases

For off-plan or VEFA purchases, timing deserves particular attention. These transactions may involve a reservation stage, a payment schedule, deed signature and later delivery of the property.

If the transaction is close to the July 2026 changeover, buyers should confirm when the deed is expected to be registered and which registration duty rate will apply.

The key point is not only whether the property is eligible for foreign acquisition. It is also whether the acquisition timeline affects the total cost.

This should be clarified early with the notary, developer and adviser involved in the transaction, especially when the purchase is planned around a fixed budget.

For off-plan purchases, our article on VEFA in Mauritius explains staged payments, deed timing and key checks before signing.

Frequently asked questions

What is registration duty in Mauritius?

Registration duty is a duty payable when certain legal documents are registered. In a property purchase, it is usually linked to the registration of the deed transferring the property to the buyer.

Do foreign buyers pay 10% registration duty in Mauritius?

From 1 July 2026, a 10% registration duty applies to certain transfers to non-citizens involving residential property under specified legal routes. It should not be treated as a blanket rule for every possible foreign-buyer transaction.

When does the 10% registration duty apply?

The 10% rate applies to in-scope transfers to non-citizens on or after 1 July 2026. Buyers should ask their notary to confirm whether their specific transaction falls within the rule.

Is registration duty the same as land transfer tax?

No. Registration duty is linked to registration of the deed and is generally part of the buyer’s acquisition-cost planning. Land transfer tax is generally associated with the seller side, although it may affect the wider transaction context.

Who confirms the registration duty payable?

The notary should confirm the registration duty payable for the specific transaction. Foreign buyers should request a full cost breakdown before signing.

A cost to clarify before committing

Registration duty in Mauritius is not just a formality. For foreign property buyers, especially those purchasing under approved residential property routes, it can significantly affect the total acquisition budget.

The 10% rate from 1 July 2026 makes timing, legal route and deed registration especially important. Buyers should therefore confirm the applicable rate early, understand the difference between registration duty and other transaction costs, and rely on transaction-specific advice before committing.

A well-prepared buyer does not only ask whether they can buy the property. They also ask what the acquisition will really cost at completion.

Considering a property purchase in Mauritius?

Our team can help you explore properties that match your investment goals, residence plans and acquisition budget.

View Available Properties | Speak to us

Sources

Economic Development Board, Amendments to IRS, RES, IHS, PDS and Smart City Regulations

Economic Development Board, FAQ on Amendments to Property Regulations

Economic Development Board, Acquisition and Lease of Immovable Property by Non-Citizens

The information contained in this article is provided for informational purposes only and reflects the situation at the time of publication. Registration duty, land transfer tax, property acquisition rules, approval requirements, deed registration procedures, rates, thresholds and transaction costs are subject to change without notice. Readers should verify all information with qualified legal, tax and property professionals and the relevant authorities before making any purchasing or investment decision. Allys and its representatives accept no responsibility for errors, omissions or changes occurring after publication.

About the Author